A credit score is a numerical representation of an individual's creditworthiness, derived from their credit history and financial behavior. It plays a crucial role in determining eligibility for loans, credit cards, and even rental agreements. Understanding credit scores is essential for making informed financial decisions, as they can significantly impact interest rates and loan terms. Many people struggle with maintaining a good credit score, which can lead to higher borrowing costs and limited access to financial products. This article will explore the fundamentals of credit scores, how they are calculated, their importance to various stakeholders, and practical strategies for improving them.

The profound impact of credit scores on financial opportunities is further underscored by research highlighting their critical role in lending decisions and the factors that shape them.

Credit Scoring: Impact on Loans, Rates & Creditworthiness

This study explores the critical role of credit scoring in determining borrowers' creditworthiness, tracing its historical evolution, applications in lending decisions, and key factors influencing credit scores. The findings confirm that credit scores significantly impact loan approvals and interest rates, with payment history and credit type diversity emerging as major determinants. The study emphasizes the interdependent relationship between borrowers and lenders, where high credit scores facilitate easier access to credit, while low scores create financial barriers.

Credit scoring: Assessing creditworthiness and its implications for borrowers and lenders, 2018

What Is a Credit Score and Why Does It Matter?

A credit score is a three-digit number that reflects an individual's creditworthiness based on their credit history. It is calculated using various factors, including payment history, amounts owed, length of credit history, new credit, and types of credit used. Credit scores typically range from 300 to 850, with higher scores indicating better creditworthiness. Understanding the significance of credit scores is vital, as they influence loan approvals, interest rates, and even employment opportunities. A good credit score can lead to lower interest rates on loans, while a poor score may result in higher costs or denial of credit altogether.

Further elaborating on the fundamental definition and common scoring models, one study highlights the FICO method's role in assessing creditworthiness.

Credit Score Definition: FICO Method & Range

Credit score is a creditworthiness index, which enables the lender (bank and credit card companies) to evaluate its own risk exposure toward a particular potential customer. There are several credit scoring methods available in the literature, but one that is widely used is the FICO method. This method provides a score ranging from 300 to 850 as a fast filter for high-volume complex credit decisions.

A fuzzy decision support system for credit scoring, J Ignatius, 2018

At Conectiv, a financial education platform dedicated to helping individuals and families make smarter financial decisions, understanding credit scores is a foundational step toward greater financial well-being. By mastering the basics, Conectiv members can take confident, informed action on loans, credit cards, and long-term wealth building.

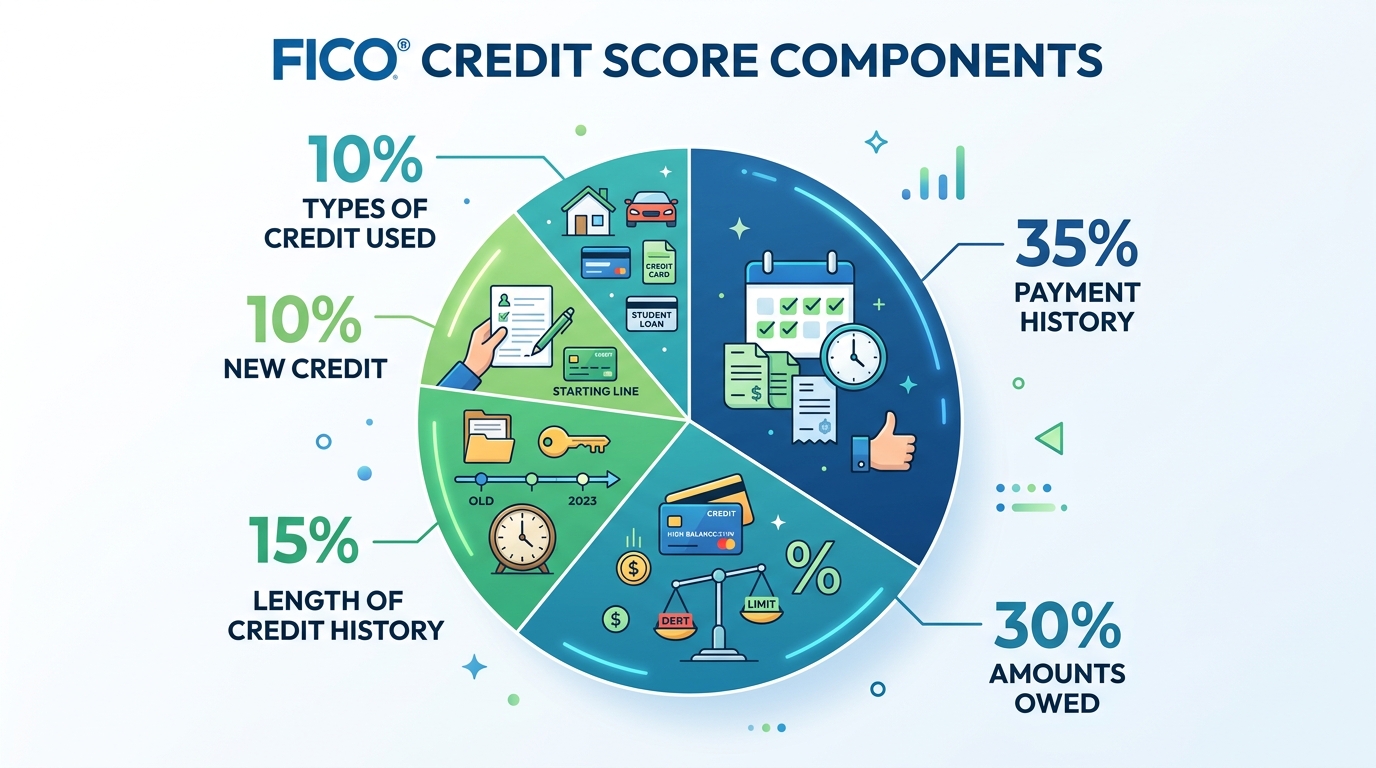

How Are Credit Scores Calculated?

Credit scores are calculated using a variety of factors that reflect an individual's credit behavior. The most common scoring model is the FICO score, which considers five key components. Alternative models such as VantageScore use similar inputs but may weight them differently, giving creditors additional tools to assess risk.

- Payment History (35%): This is the most significant factor, reflecting whether payments have been made on time.

- Amounts Owed (30%): This includes the total amount of debt and the credit utilization ratio, which is the percentage of available credit being used.

- Length of Credit History (15%): A longer credit history can positively impact the score, as it provides more data on credit behavior.

- New Credit (10%): This factor considers recent credit inquiries and the number of new accounts opened.

- Types of Credit Used (10%): A mix of credit types, such as credit cards, mortgages, and installment loans, can enhance a credit score.

Understanding these components can help individuals identify areas for improvement in their credit profiles.

Key Components of Credit Score Calculation Explained

The calculation of credit scores involves several critical components that contribute to the overall score. Here's a breakdown of these components:

Component | Description | Impact on Score |

|---|---|---|

Payment History | Tracks on-time payments and delinquencies. | High |

Amounts Owed | Reflects total debt and credit utilization ratio. | High |

Length of Credit History | Considers the age of credit accounts and the average age of accounts. | Medium |

New Credit | Looks at recent credit inquiries and newly opened accounts. | Low |

Types of Credit Used | Evaluates the variety of credit accounts held. | Medium |

This table illustrates how each component contributes to the overall credit score, highlighting the importance of maintaining a positive payment history and managing debt levels effectively. Credit bureaus such as Equifax, Experian, and TransUnion collect this data and supply it to scoring models to generate your score.

Who Uses Credit Scores: Investors, Companies, and Consumers

Credit scores are utilized by various stakeholders, including investors, companies, and consumers. Investors often assess credit scores to evaluate the risk associated with lending to individuals or businesses. Companies, particularly financial institutions, rely on credit scores to determine the creditworthiness of potential borrowers, influencing their lending decisions. Consumers, on the other hand, use credit scores to understand their financial standing and make informed decisions regarding loans, credit cards, and other financial products. Creditors of all types — from banks to credit unions — use these scores as a primary filter in the approval process.

Specifically, for financial institutions, managing credit risk is a paramount concern, and credit scoring strategies are central to this effort.

Credit Scoring for Financial Institutions & Risk Management

This credit risk is a major concern for financial institutions in today's world. Thus, the main objective of this paper is to provide an empirical study on credit risks faced by the financial institutions and the credit risk management employing credit scoring strategies. These strategies clearly estimate the creditworthiness and trustworthiness of the customers belonging to the financial institutions.

An empirical study on credit scoring and credit scorecard for financial institutions, MSI Ahmed, 2019

Understanding who uses credit scores and why can empower individuals to take control of their financial health and improve their credit profiles.

How Credit Score Ranges Affect Loan and Credit Approvals

Credit score ranges play a crucial role in determining loan and credit approvals. Generally, scores are categorized as follows:

- Excellent (750–850): Borrowers in this range typically qualify for the best interest rates and terms.

- Good (700–749): Individuals with good credit scores can still access favorable loan options, though rates may be slightly higher.

- Fair (650–699): Borrowers may face higher interest rates and stricter lending criteria.

- Poor (600–649): Individuals in this range may struggle to secure loans and could face significantly higher rates.

- Very Poor (below 600): Borrowers may be denied credit altogether or offered loans with exorbitant interest rates.

Understanding these ranges can help individuals gauge their credit health and take necessary steps to improve their scores.

How Can You Improve Your Credit Score? Practical Tips and Strategies

Improving your credit score is achievable with consistent effort and strategic planning. Here are some practical tips to enhance your credit profile:

- Make Timely Payments: Ensure all bills and debts are paid on time to maintain a positive payment history.

- Reduce Credit Utilization: Aim to keep your credit utilization below 30% of your total available credit.

- Avoid Opening New Accounts Frequently: Limit the number of new credit inquiries, as too many can negatively impact your score.

- Monitor Your Credit Report: Regularly check your credit report for errors and dispute any inaccuracies.

- Diversify Your Credit Mix: Consider having a mix of credit types, such as revolving credit and installment loans, to improve your score. A line of credit, for example, can contribute positively to your credit mix when managed responsibly.

By implementing these strategies, individuals can work towards achieving a healthier credit score and better financial opportunities.

Monitoring Your Credit Report Components for Better Scores

Monitoring your credit report is essential for maintaining a good credit score. Key components to focus on include:

- Payment History: Regularly check for any missed or late payments that could impact your score.

- Credit Utilization: Keep track of your credit card balances to ensure they remain within a healthy range.

- Credit Inquiries: Be aware of how many times your credit report has been accessed, as excessive inquiries can lower your score.

Utilizing tools and services that provide credit monitoring can help individuals stay informed about their credit status and make timely adjustments.

How Do ESG Metrics Influence Credit Risk and Scoring?

Environmental, Social, and Governance (ESG) metrics are increasingly influencing credit risk assessments and scoring. These metrics provide insights into a company's sustainability practices and ethical governance, which can impact its financial stability and creditworthiness. Investors and lenders are beginning to consider ESG factors when evaluating potential borrowers, recognizing that companies with strong ESG practices may pose lower risks.

As the focus on sustainability grows, understanding how ESG metrics affect credit scoring will become increasingly important for both consumers and businesses. This shift highlights the need for individuals to be aware of their financial health in the context of broader societal trends.

ESG Metric | Impact on Credit Risk Assessment | Importance Level |

|---|---|---|

Environmental Practices | Companies with strong practices may face lower risks. | High |

Social Responsibility | Positive social impact can enhance reputation and stability. | Medium |

Governance Standards | Strong governance can lead to better financial performance. | High |

Start Building a Stronger Credit Foundation Today

Credit scores are not fixed — they reflect your financial habits over time, and they can always be improved with the right knowledge and consistency. Whether you're working to qualify for a better interest rate, secure a loan, or simply gain more control over your financial life, understanding the fundamentals covered in this guide is the first step. Conectiv's financial education platform is built to give everyday people the tools, courses, and community support to take their financial literacy further. As a Conectiv representative group, Wire Clarity connects members to expert-led education, real-time trading tools, and actionable market insights. Reach us anytime at info@wireclarity.com or call (770) 628-5463.